Q4 FY19 Results Update and Frequently Asked Questions

Q1. What is ITC's Vision and Mission?

Answer:

Vision:

Sustain ITC’s position as one of India’s most valuable and admired corporations through world-class performance, creating growing value for the Indian economy and the Company’s stakeholders.

Mission:

To enhance the wealth generating capability of the enterprise in a globalising environment, delivering superior and sustainable stakeholder value.

Q2. How does the Company effectively manage a highly diversified business portfolio? What is the Company’s Corporate Governance structure?

Answer:ITC’s ‘Strategy of Organisation’ is crafted in a manner that enables focus on each business while harnessing the diversity of the portfolio to create unique sources of competitive advantage. Please refer to the following link https://www.itcportal.com/about-itc/values/index.aspx#sectionb4 for details of ITC’s Governance Structure.

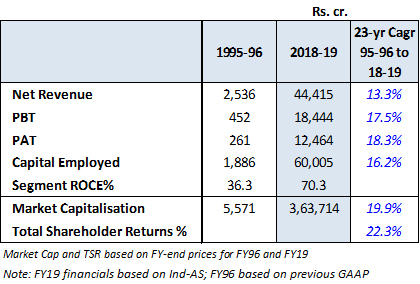

Q3. What is the Company’s shareholder value creation track record?

Answer:ITC has been a consistent performer in terms of shareholder value creation. During the period 1995-96 to 2018-19, Total Shareholder Returns have clocked compound annual growth rate of 22.3% significantly outperforming the Sensex (11.2%).

Q4. Please provide a brief overview of FY19 results.

Answer: The Company delivered another year of resilient performance despite a challenging operating environment. The Cigarettes Business, impacted by steep increase in taxes under the GST regime, sharpened focus on delivering world-class products through continuous innovation along with best-in-class execution thereby consolidating its market standing. Amidst a subdued demand environment, the non-cigarette FMCG segment grew ahead of the industry recording robust growth in revenue and significant improvement in profitability despite heightened competitive intensity, elevated input costs, gestation costs of new products/categories & manufacturing facilities and ongoing restructuring of Lifestyle Retailing Business. The Hotels Business delivered robust performance driven by improvement in RevPar and addition of two world-class properties to its portfolio. The Paperboards, Paper and Packaging segment had a stellar year recording strong growth in revenue and profits on the back of capacity addition, product mix enrichment, strategic investments in pulp import substitution, process innovation and cost-competitive fibre chain. While the Agri Business posted healthy growth in revenue, leaf cost escalation pertaining to the Andhra 2017 crop and business mix weighed on margins.

On a comparable basis, Gross Sales Value (net of rebates/discounts) for the year stood at Rs. 75309.36 crores, representing a growth of 12.3% over 2017-18 driven mainly by Agri Business, Branded Packaged Foods, Education & Stationery Products Business, Hotels and Paperboards. Excluding exceptional items, Profit Before Tax and Profit After Tax grew by 12.2% and 13.8% respectively.

Profit After Tax at Rs. 12464.32 crores registered growth of 11.1% during the year. Total Comprehensive Income for the year stood at Rs. 12826.88 crores (previous year Rs. 11605.59 crores). Earnings Per Share for the year stood at Rs. 10.19 (previous year Rs. 9.22).

Q5. (a). Why has ‘Consumption of Raw Material etc. (net)’ increased by Rs. 1515 Crores during FY19 as compared to FY18?

Answer:Increase in Consumption of Ram Material is mainly due to higher share of agri business in sales. On a comparable basis, adjusting for the higher share of agri business, the increase in cost is in line with growth in revenue.

Q5. (b). Why has ‘Other Expenditure’ increased by about Rs. 847 Crores from Rs. 6809.06 Crores in FY18 to Rs. 7656.55 Crores in FY19?

Answer: Increase in Other Expenditure is mainly attributable to higher freight expenses mainly on account of agri business coupled with increase in fuel costs and increase in operating expenditure on account of new facilities.

Q5. (c). What is the growth in FMCG - Others - Segment EBITDA in FY19 as compared to FY18?

Answer: In respect of FMCG-Others segment, earnings before interest, taxes, depreciation and amortization (EBITDA), for FY19 is at Rs. 688.2 Crores representing a growth of 51.1% driven by enhanced scale and product mix enrichment.

Q6. Please provide a revenue split of the FMCG–Others Segment.

Answer:The Branded Packaged Foods Businesses represent the largest component of this segment, accounting for ~77% of Segment Revenue. The Personal Care Business and Education and Stationery Products Business account for ~8% and ~7% each of Segment Revenues respectively.

Q7. What are the new FMCG categories that the Company is likely to enter over the short to medium term?

Answer: With aspirations to become the No.1 FMCG player in India, the Company continuously evaluates opportunities to grow in the FMCG space.

The choice of category is guided by its growth prospects, profitability profile and the ability of the Company to effectively leverage its institutional strengths with a view to achieving leadership status within a reasonable time frame. Synergies with existing categories in terms of overlap of distribution reach, brand extension possibility, procurement efficiencies etc. are considered while choosing new categories.

The Company is in the process of scaling up its presence in Dairy & Beverages, Chocolates, Coffee and Frozen Snacks.

Q8. What is the margin profile of the Branded Packaged Foods Business?

Answer:The Branded Packaged Foods Businesses of the Company comprise ‘Confections’, ‘Staples, Snacks and Meals’ and ‘Dairy & Beverages’. These Businesses have evolved over a period of time and are currently at different stages of their lifecycles. As such, the revenue dimensions, cost structures and profitability profiles of each of these businesses are distinct from the other. For example, EBIT margin is in the high single digit range for the Staples business (first full year of launch: 2002/03) while the same is in the mid-single digit range for the Snack Foods business (first full year of launch: 2007/08) representing upfront investments towards category development and brand building.

Overall, each category is striving towards achieving best-in-class margins within a reasonable period of time.

Q9. What is the margin profile of the Personal Care Products Business? When will it break-even?

Answer: The Personal Care Products Business presently comprises the ‘Personal Wash & Hygiene’, ‘Fragrances’, ‘Home Care’, ‘Skin Care’, ‘Health’ and ‘Talc’ categories. The Company continues to make significant investments in this Business primarily in the area of brand building, R&D and product development towards competing effectively with incumbent players comprising firmly entrenched MNCs and domestic companies.

Presently, each category is operating at industry benchmarked gross margins. With enhanced scale and consumer connect, each category is expected to earn best-in-class EBIT margins progressively over the medium-term.

Q10. What are the Company’s targets in the FMCG–Others space? What does the Company envision in terms of revenue and profits in this segment, over the medium and long-term?

Answer:ITC’s endeavour is to become the No.1 FMCG player in India driven by the existing portfolio as well as entry into new categories. In this regard, the Company is aiming for revenue of Rs. 100,000 Crores from the new FMCG businesses by the year 2030.

Over the medium term, the Company seeks to grow revenues of each category within the FMCG-Others segment at a rate which is well ahead of industry. With enhanced scale and consumer connect, each category is expected to earn best-in-class EBIT margins, progressively over the medium-term.

Q11. Would ITC contemplate acquisitions in order to achieve its vision in the Other FMCG segment?

Answer:ITC examines prospects for inorganic growth that arise from time to time not only in this business segment but also in the other businesses. The Company continues to evaluate opportunities to grow its businesses through Acquisitions and Joint Ventures and is guided by considerations such as strategic fit, valuation, financial viability, ease of integration etc.

The Company’s ‘Savlon’ and ‘Shower to Shower’ brands, acquired earlier, have been leveraged to strengthen its position in the personal care space by expanding its existing product portfolio and gaining access to newer consumer segments and markets. The offerings have garnered significant consumer franchise and are well poised for rapid growth.

‘Charmis’ brand acquired by the Company in FY18 has been leveraged to re-launch moisturising skin creams with a fresh look & enhanced sensorial experience supported by a focussed campaign showcasing the brand’s core value proposition - ‘it is the goodness within that glows on the face’.

Earlier during the year, Personal Care Products Business forayed into the floor cleaner segment under the recently acquired ‘Nimyle’ brand. The range of herbal floor cleaners was extended to new markets even as it recorded robust growth in existing markets. Plans are on the anvil to scale up the brand’s presence across target markets.

Q12. Please provide an update on the Company’s progress in the FMCG-Others Segment during the year.

Answer:After continued sluggishness over the last two years, which witnessed two major economic reforms – demonetisation of Specified Bank Notes and Goods and Services Tax, there was anticipation of significant pick up in the FMCG industry. However, after a promising first half, growth in the second half of the year particularly in the last 3-4 months was muted due to tight liquidity conditions and sluggish rural demand.

Despite the challenging conditions prevailing during the year, FMCG-Others Segment Revenue at Rs. 12505.28 crores grew ahead of industry and recorded an increase of 12% (on a comparable basis and excluding the impact of ongoing restructuring in Lifestyle Retailing Business). Most major categories enhanced their market standing during the year. While ‘Bingo!’ snacks, ‘Aashirvaad’ atta, ‘YiPPee!’ noodles and ‘Dark Fantasy Choco Fills’ super-premium cream biscuits were the key drivers of growth in the Branded Packaged Foods Businesses, ‘Engage’ deodorants, ‘Vivel’/‘Fiama’ shower gels & bodywash and ‘Savlon’ handwash reported robust growth in the Personal Care Products Business. The Education and Stationery Products Business posted a strong performance during the year led by ‘Classmate’ notebooks, which consolidated its leadership position in the industry.

As part of the ongoing restructuring of the Lifestyle Retailing Business, the Company divested the ‘John Players’ trademark/copyright and its variants in the apparel category along with related goodwill. Segment Results for the year (excl. net gain on restructuring of Lifestyle Retailing Business) posted significant improvement to Rs. 315.72 crores from Rs. 164.12 crores in 2017-18. This was driven by enhanced scale, product mix enrichment and strategic cost management initiatives after absorbing the impact of sustained investment in brand building, gestation costs of new categories & facilities and costs associated with the ongoing structural interventions in the Lifestyle Retailing Business.

During the year, the Company commissioned a world-class Integrated Consumer Goods Manufacturing and Logistics Unit (ICML) at Pudukkottai (Tamil Nadu) while operations at Kapurthala (Punjab), Panchla (West Bengal), and Guwahati (Assam) were further ramped up. Significant progress was also made in constructing several other state-of-the-art owned ICMLs across regions towards supporting the rapid scale-up plans in the FMCG Businesses.

Against the backdrop of a challenging operating environment as aforestated, the Company sustained its position as one of the fastest growing branded packaged foods businesses in the country, leveraging a robust portfolio of brands, a slew of first-to-market offers, a range of distinctive products customised to address regional tastes and preferences along with an efficient supply chain and distribution network. The Business implemented several initiatives encompassing cost management, supply chain optimisation, smart procurement, alternative fuel usage and productivity improvement through automation which helped in absorbing escalation in input costs, start-up costs of new facilities and strategic investments in brand building for new categories viz. Dairy, Juices, Chocolates and Coffee.

In the Staples Business, ‘Aashirvaad’ atta fortified its market standing across geographies and its leadership position in the industry.

Supported by its new positioning that it is sun-dried and made from natural sea salt crystals, backed up by on ground activations, visibility and media investments, Aashirvaad salt gained traction in key geographies and posted strong performance during the year. In the branded Spices category, the Aashirvaad range of spices registered robust revenue growth.

In the Snacks and Meals Business, the ‘Bingo!’ range of snacks recorded robust growth during the year driven by new product launches, portfolio renovation and extensions, expansion of distribution footprint, tailor-made trade marketing support and consistent & impactful communication. Bingo! sustained market leadership in the bridges segment and Tedhe Medhe emerged as India’s most distributed brand in the category. The Business strengthened its product range with the launch of some innovative variants such as Mad Angles Very Peri Peri, Mad Angle Fillos & Tedhe Medhe Wakhra Style. These products have garnered encouraging consumer traction and are being rolled out to other markets. Bingo! potato chips recorded impressive market share gains and consolidated its leadership position in the South. Bingo! No Rulz, launched in the previous year, continued to gain consumer franchise with its unique value proposition of multiple shapes in a single pack.

In the Instant Noodles category, ‘YiPPee!’ noodles sustained its growth momentum during the year despite increasing competitive intensity from national and several regional discount players. The Business continued to focus on premiumising its product portfolio and enhancing brand affinity. During the year, the Business launched limited edition variants under the ‘My’ range sub-brand. Available in four exciting variants, the range has been crafted keeping in mind the taste preferences of young adults and has received good response from consumers.

The Confections Business continued to pursue portfolio premiumisation and augment its range with the introduction of low unit packs and channel-specific SKUs to its assortment. In the Biscuits category, the Business consolidated its leadership position in the Super-Premium segment with continued focus on enhancing brand affinity, strengthening the supply chain and expanding distribution reach. Consistent and impactful communication, coupled with focused marketing inputs helped improve penetration and brand heath metrics. ‘Dark Fantasy Choco Fills’ witnessed further acceleration in growth momentum driven by superior product attributes, focused communication and consumer activation. During the year, the Business augmented its portfolio in the rapidly growing Cakes segment through the launch of Layered cakes under the ‘Sunfeast’ Bounce brand and expanded the offerings in the Marie & Cookies segment with the launch of Sunfeast Marie Light Vita & Sunfeast Mom’s Magic Choco Chip Cookies. Various innovative and first-to-market launches such as Bounce Minifills and Dark Fantasy Jellifills also led to premiumising the portfolio. Tailored and contextual content on digital platform were deployed to enhance reach and drive brand imagery.

In the Confectionery category, the Business continued to focus on premiumising its product portfolio with its differentiated and unique offerings at “Rupee 1 and above” price point with greater thrust on Multi-unit pack portfolio. During the year, the Business augmented its portfolio with the launch of Chatpata Tadka Time, a unique first to market format of masala coated jelly beans and forayed into bridged chocolate segment with the launch of ‘Candyman’ Fantastik, an offering of wafer sticks filled with chocolate crème filling. These products have received encouraging consumer response.

In the Dairy & Beverages Business, the 'B Natural' range of juices leveraged its 'Not from Concentrate' platform to deepen consumer connect by providing a more nutritive and ‘natural’ tasting experience whilst simultaneously promoting fruit pulp procured from Indian farmers, thereby supporting the Indian farm and food processing sector. The entire range of B Natural Beverages is ‘made with 100% Indian Fruit & 0% concentrate’. The Business also launched premium range of juices comprising Ratnagiri Alphonso, Himalayan Mixed Fruit and Dakshin Guava in an appealing transparent bottle format providing an exotic & rich fruit experience which has received an excellent initial response from the target consumers. In the Dairy segment, Business extended Aashirvaad pouch milk to Kolkata and Patna and scaled up presence in existing markets. This has received excellent response in relatively short period of time. ‘Aashirvaad Svasti’ Ghee continues to gain consumer traction and excellent product feedback from the limited markets where it has been launched. The Aashirvaad Svasti portfolio was augmented with the introduction of pouch curd and paneer. The Business also forayed into the Dairy Beverages segment with the launch of four differentiated variants of milkshakes under the 'Sunfeast Wonderz' brand with distinctive positioning – initial consumer response has been encouraging.

In the Chocolates category, the Business launched a range of premium chocolate bars crafted in 2 unique product formats – Fabelle ‘Soft Centres’ (centre filled chocolate bars) and Fabelle ‘Choco Deck’ (layered chocolate bars) in select markets, which is gaining consumer traction. Presence in the luxury segment portfolio was strengthened by leveraging the world-class Fabelle boutiques, new launches in the boxed chocolate segment and continued communication across key digital media. In the boxed chocolate range, the Business launched India’s first Ruby Chocolate, Ruby Gianduja. ‘Sunbean’ gourmet coffee, which is available across all ITC Hotels, continues to receive excellent response from discerning consumers. The Business is also piloting ready-to-use beaten instant coffee paste in select markets.

The Personal Care Products Business delivered a healthy performance during the year and continued to enhance its market standing in the Hand Hygiene, Fragrance, Body Wash and Skin Care categories. This was driven by sustained focus on innovation, portfolio premiumisation, expansion of distribution reach and proactive cost management.

In the Fragrance category, ‘Engage’ recorded impressive gains, consolidating its leadership position in the women’s segment and No. 2 position overall. The Business continues to garner consumer traction in the fast-growing small pack format of pocket perfumes and rapidly grew volumes despite intense competition.

In the Personal Wash category, new bar soap variants such as ‘Vivel’ Cool received positive consumer response in the markets of launch. In the bodywash segment, ‘Fiama’ continued to garner increasing consumer franchise. During the year, the Business introduced Vivel Bodywash in select markets at an attractive price point to offer bar soap users an enhanced bathing experience. ‘Savlon’ handwash recorded significant gains during the year across brand health metrics and emerged as one of the fastest growing brands in the market.

The Business strengthened its presence in the Skincare space with the launch of ‘Dermafique’ range of premium skincare products which have been developed at the Company’s state-of-the-art Life Sciences and Technology Centre leveraging the latest breakthroughs in bioscience, nanotechnology and derma science. Designed and validated for the Indian consumer, the innovative premium range of products include anti-ageing, specialised hydrating creams, body serum, cleansing and toning products. In the popular Skincare space, the Business restaged ‘Charmis’ skin cream with a fresh look & enhanced sensorial experience supported by a focussed marketing campaign. The new product innovations and launches in the Skincare space have received encouraging response from target consumers.

Several new and exciting consumer friendly offerings were launched during the year, which include Savlon Hand Sanitiser in a child-friendly pen format and Savlon Antiseptic Liquid in a “Braille” pack for the visually impaired.

During the year, the Business forayed into the Floor Cleaner market with the recently acquired ‘Nimyle’ brand. Leveraging its 100% natural brand positioning, Nimyle has attained leadership position in West Bengal and is being extended to other parts of India.

During the year, the Stationery industry witnessed heightened competitive intensity along with a sharp escalation in paper prices. Despite these challenging conditions, the Business posted robust growth in revenue and sustained its leadership position in the industry anchored on a portfolio of world-class products and brands and an efficient distribution network.

During the year, the product portfolio was augmented with the launch of several new products including paper and filing solutions, range of vibrant colour options and gift packs under the ‘Paperkraft’ portfolio and several offerings in the pens category. The Business also scaled up presence in the value segment of the notebook industry through the ‘Saathi’ brand with a view to consolidating its leadership position.

The Agarbatti category witnessed premiumisation with consumers seeking better product experience and more culturally relevant fragrances. Apart from introduction of newer formats and modern fragrances, the industry witnessed aggressive media and promotion spends to garner higher market share. Notwithstanding such competitive intensity, Mangaldeep’s household penetration increased in urban & rural markets during the year in both the Agarbatti and Dhoop formats. The brand sustained its position as the second largest brand in the Agarbatti category and leader in the Dhoop segment.

While demand conditions in the Safety Matches industry remained sluggish, the Business sustained its market leadership position through portfolio premiumisation and by leveraging a portfolio of offerings across market segments. ‘AIM’ continues to be the largest selling brand in the industry.

The Business continued to execute the structural interventions initiated in the previous year across the value chain including restructuring its retail foot print and rationalising the store network, modifying the design language of its offerings, restructuring the terms of trade with business partners and sharpening working capital management. During the year, the Company divested the ‘John Players’ trademark/copyright and its variants in the apparel category along with related goodwill.

Please refer to the FMCG - Others section in the Report of the Directors & Management Discussion and Analysis for the financial year ended 31st March 2018 and Media Releases on quarterly results for further details.

Q13. What is the progress on upcoming integrated consumer goods manufacturing facilities (ICMLs) of the Company?

Answer: The Company continues to make investments in Integrated Consumer Manufacturing Facilities (ICMLs) towards augmenting the manufacturing and sourcing footprint across categories with a view to improving market responsiveness, leveraging fiscal incentives and reducing the cost of servicing proximal markets. During the year, the Company commissioned a world-class Integrated Consumer Goods Manufacturing and Logistics Unit (ICML) at Pudukkottai (Tamil Nadu) while operations at Kapurthala (Punjab), Panchla (West Bengal), and Guwahati (Assam) were further ramped up. Significant progress was also made in constructing several other state-of-the-art owned ICMLs across regions towards supporting the rapid scale-up plans in the FMCG Businesses. These ICMLs are expected to set new benchmarks leveraging scale over a period of time and improving cost efficiencies while ensuring best-in-class product quality.

Q14. Please provide an update on the Cigarettes business.

Answer:A punitive and discriminatory taxation and regulatory regime, together with sharp increase in illegal trade in recent years, continue to pose significant operating challenges to the legal cigarette industry in the country.

Contrary to indications from the Government that the transition to GST would be based on principles of maintaining revenue neutrality, tax incidence on cigarettes have risen sharply under the GST regime and the discrimination vis-à-vis other tobacco products continues. The legal cigarette industry, already reeling under the cumulative impact of steep increase in taxation over the previous five years in pre-GST regime and intense regulatory pressures, was further impacted by a sharp increase of 13% in tax incidence on cigarettes (19% increase for the king-size filter segment) under the GST regime. Coupled with the increase in Excise Duty rates announced in the Union Budget 2017, this resulted in an incremental tax incidence of over 20% on cigarettes, post implementation of GST.

It is pertinent to note that the tax incidence on cigarettes has nearly trebled between 2011-12 and 2017-18, on a comparable basis and cigarette taxes are effectively about 55 times higher than taxes on other tobacco products on a per kg basis. Excessive taxation has made legal, duty-paid cigarettes in India amongst the costliest in the world in terms of per capita affordability.

The high rates of tax on cigarettes provide attractive tax arbitrage opportunities for illicit trade allowing sale of these cigarettes to consumers at prices much lower than those of duty-paid domestic cigarettes. This has encouraged mushrooming of unscrupulous operators who indulge in clandestine manufacturing of cigarettes across the country and also provided a huge impetus to large-scale smuggling of international brands into the country. Seizure of large quantum of smuggled cigarettes by enforcement agencies across the country over the recent years confirm the growing menace of illegal cigarette trade in the country. While the legitimate cigarette industry has declined steadily since 2010-11 at a compound annual rate of over 4% p.a., illegal cigarette volumes in contrast have grown at nearly 5% p.a. during the same period, making India one of the fastest growing illegal cigarette markets in the world. It may be noted that, according to Euromonitor International, India is now the 4th largest illegal cigarette market in the world.

The disparity in taxation on tobacco products has caused a progressive migration from consumption of duty-paid cigarettes to other lightly-taxed / tax evaded forms of tobacco products, comprising illegal cigarettes and bidi chewing tobacco, gutkha, zarda, snuff, etc. As a consequence, while the share of legal cigarettes in total tobacco consumption in the country has declined considerably over the years, aggregate tobacco consumption has increased over the same period. The cost disadvantage faced by duty-paid cigarettes as compared to illegal cigarettes is exacerbated by the fact that duty-paid cigarettes comply fully with provisions of applicable Indian legislation like The Cigarettes and Other Tobacco Products (Prohibition of Advertisement and Regulation of Trade and Commerce, Production, Supply and Distribution) Act, 2003 (COTPA) and bear the statutorily mandated pictorial and textual warnings covering 85% of the surface area of the packet (one of the largest in the world). On the other hand, the smuggled illegal cigarettes do not bear any such pictorial or textual warnings or bear much smaller pictorial warnings as per the tobacco laws of the countries from where these cigarettes are sourced. As reported in prior years, findings from research conducted by IMRB International, an independent market research organisation, show that the lack of pictorial warnings on packets of smuggled cigarettes or their diminutive size creates a perception in the consumer’s mind that smuggled cigarettes are ‘safer’ than domestic duty-paid cigarettes that carry the 85% pictorial warnings. Along with low prices to consumers (enabled through tax evasion), this has opened the floodgates for contraband cigarettes.

Significantly, several other major tobacco producing countries, including the USA have framed regulatory frameworks for tobacco taking into consideration the interests of their tobacco farmers and in deciding whether or not to adopt large or excessive pictorial warnings. The inadvertent and unforeseen consequence of the stringent Indian tobacco regulations is one of continuing losses to the Indian tobacco farmer with corresponding gains to tobacco farmers in the countries that have opted for moderate and equitable tobacco regulations. These developments have had a devastating impact on the Indian tobacco farmer and the 46 million livelihoods dependent on the tobacco value chain.

As reported last year, the Company and several other stakeholders had challenged the validity of the pictorial warnings. The Karnataka High Court, by its judgement in December 2017 held the 85% pictorial warnings with extremely gruesome imagery to be factually incorrect and unconstitutional. Upon a Special Leave Petition filed by the Government, the Honourable Supreme Court has stayed the Order of the High Court. Pending the final hearing of this matter, the regime of the extremely repugnant 85% pictorial warnings continues. In fact, new pictorial warnings with even more gruesome images have been introduced from 1st September 2018.

In India, cigarettes are manufactured largely using flavourful Flue Cured Virginia Tobacco (FCV) which is grown in the States of Andhra Pradesh, Telangana and Karnataka. As smuggled international brands of cigarettes do not use Indian tobaccos, the growth of the illegal cigarette trade has resulted in a drop in demand for Indian FCV tobaccos, in addition to revenue losses. Stable domestic demand would enhance the ability of the Indian tobacco farmer to weather the instabilities of the international market. Continuous decline in domestic demand has instead sub-optimised earnings of the Indian farmers from tobacco crop exports as well. All this has only served to increase the plight of the Indian tobacco farmers. It is estimated that in the four years since 2013-14, Indian tobacco farmers have suffered a cumulative drop in earnings of a staggering Rs. 4,061 crore.

Due to sharp increase in the tax incidence post transition to GST regime, there was a steep decline in legal industry volumes in 2017-18. Legal cigarette industry remains under severe pressure due to the cumulative impact of increase in tax incidence over the last five years. Stability in taxes during the year provided some relief to the legal cigarette industry. However, it is pertinent to note that the legal cigarette industry volumes remain significantly below June’14 levels.

The Company’s unwavering focus on nurturing a portfolio of world-class products, superior consumer insights and a strategy of continuous innovation and value creation helped deliver superior competitive performance. Deep consumer insights and a robust innovation pipeline enabled the Business to introduce new variants catering to the continuously evolving consumer preferences. These include Classic Rich & Smooth, Classic Verve Low Smell and Gold Flake NEO which have received positive response in the market. Similarly, recently introduced brands/variants such as American Club, Players and Wave strengthened their market standing during the year.

Please refer to the FMCG - Cigarettes section in the Report of the Directors & Management Discussion and Analysis for the financial year ended 31st March 2018 and Media Releases on quarterly results for further details.

Q15. What is the Company’s view on cigarette volume trends over the medium to long term?

Answer: As aforestated, tax incidence on cigarettes has nearly trebled between 2011-12 and 2017-18, on a comparable basis and taxes on cigarettes are effectively about 55 times higher than taxes on other tobacco products on a per kg basis. Excessive taxation has made legal, duty-paid cigarettes in India amongst the costliest in the world in terms of per capita affordability.

As highlighted earlier, while overall tobacco consumption in the country continues to grow, the share of duty-paid cigarettes has come down substantially over the years and is estimated to account for around 10% of current tobacco consumption in the country. Despite accounting for such a low share of overall tobacco consumption in the country, the legal cigarette industry contributes more than 86% of tax revenue from the tobacco sector. The other types of tobacco products contribute barely 14% of tax revenues from the tobacco sector despite accounting for 90% of total tobacco consumption.

While this indicates room for growth in legal cigarette volumes going forward, this would largely depend on the taxation and regulatory policy on cigarettes adopted by the Government. Such growth potential was demonstrated during the period 2004/05 to 2006/07 and again, more recently, in 2009/10 and 2011/12 – years in which taxes / duties growth were moderate.

As in the past, the Company continues to represent with policy makers for equitable, non-discriminatory, pragmatic, evidence-based regulations and taxation policies that balance the economic imperatives of the country and the tobacco control objectives, having regard to the unique tobacco consumption pattern in India. Due to sharp increase in the tax incidence post transition to GST regime, there was a steep decline in legal industry volumes in 2017-18. Legal cigarette industry remains under severe pressure due to the cumulative impact of increase in tax incidence over the last five years. Stability in taxes during the year provided some relief to the legal cigarette industry. However, it is pertinent to note that the legal cigarette industry volumes remain significantly below June’14 levels. Moderation in taxes is critical for addressing the interests of all the stakeholders of this industry, including the tobacco farmers, the exchequer and the consumers.

Q16. At what rate are Cigarettes taxed under the GST regime? What is the impact of GST on Cigarettes Business?

Answer:Cigarettes are taxed under the GST regime at the peak rate of 28%. Additionally, a GST Compensation Cess which includes an Ad Valorem component and a Specific Tax component based on cigarette length, has also been imposed. The National Calamity Contingent Duty (NCCD) component of Excise Duty continues to be levied as earlier based on the length of the cigarette.

Q17. What is the impact of the larger graphic health warnings (GHW) on packs on the cigarette industry?

Answer: The 85% GHW is excessively large, extremely gruesome and unreasonable. There is no evidence that cigarette smoking would cause the diseases depicted in the pictures or that large GHW will lead to reduction in consumption. The large GHW fuels the growth of smuggled international brands as such cigarette packs do not carry the excessively large (85% of the surface area of both sides of the cigarette package) pictorial warnings with extremely gruesome and unreasonable images that are prescribed under Indian laws. While the legal cigarette industry scrupulously complies with the statutory provisions, smuggled international brands of cigarettes either do not bear any pictorial or other health warnings or bear warnings of much smaller dimensions, that too different from what is mandated under Indian law. Findings from research conducted by IMRB International, an independent organisation, indicate that the lack of warnings or their diminutive size creates a perception in the consumer’s mind that the smuggled cigarettes are ‘safer’ than domestic duty-paid cigarettes that carry the statutory warnings. As stated earlier, new graphic health warnings with even more gruesome images have been introduced from 1st September 2018.

It is pertinent to note that the global average size of pictorial warnings is only about 30% coverage of the principal display area. In fact, the three countries that account for about 51% of the world’s cigarette consumption, viz., USA, Japan and China have not adopted pictorial / graphical warnings and have prescribed only text-based warnings on cigarette packages. The statutorily prescribed pictorial warning occupying 85% of both sides of a cigarette pack ranks India in the 2nd position globally in terms of their stringency Unfortunately, these laws have fuelled, albeit unintentionally, the growth of illegal cigarettes in the country.

The excessively large GHWs prevent consumers from making an informed choice in a competitive market, since they are denied adequate information about the brand on the cigarette packages. The Company believes that such GHW also devalues the Intellectual Property Rights of brand owners and sub-optimises the large investments made over the years in creating and nurturing the brands.

Q18. What are the Company’s plans in the ‘Electronic Nicotine Delivery Systems (ENDS)’ space?

Answer: 'Electronic Nicotine Delivery Systems (ENDS)’ broadly refer to both Electronic Vaping Devices (EVD), commonly called ‘e-cigarettes’ as well as ‘electronic Heat Not Burn (eHNB)’ products. As many as 27 countries including Singapore, Australia, Thailand, Taiwan, UAE, Brazil and Argentina have prohibited ENDS. In India, 12 States have prohibited or restricted this category. Regulatory issues are also being contested in Indian courts. Your Company’s EON brand in the EVD segment is being marketed in select states. Your Company is closely following the regulatory developments, while initiating appropriate investments, enhancing capability and gearing up to be in a state of readiness in this emerging segment.

Q19. Please provide an update on the Company’s Hotels business.

Answer: Segment Revenue recorded robust growth driven by increase in average room rates, improvement in occupancy and higher Food & Beverage revenue from existing hotels and addition of new properties to the portfolio. Improved operating leverage, notwithstanding gestation costs of newer hotels in the portfolio boosted profitability.

In view of the long-term potential of the Indian hospitality sector, the Company remains committed to enhancing the scale of the Business by adopting an ‘asset-right’ strategy that envisages building world-class tourism assets for the nation and growing the footprint of managed properties by leveraging its hotel management expertise. During the year, the Business commissioned ITC Kohenur, Hyderabad. Strategically situated in the heart of the HITEC city, in close proximity to the central business & commercial district, the hotel offers the finest accommodation and dining experiences. In its first year of operations, the hotel has been able to establish a pre-eminent position in luxury hospitality landscape of Hyderabad. The Business made steady progress during the year in the construction of luxury hotels at Kolkata and Ahmedabad. Construction of ITC Royal Bengal in Kolkata is nearing completion and is expected to be commissioned in the first quarter of 2019-20.

As reported earlier, on 19th March, 2018, the Honourable Supreme Court upheld the sale of the 250-room luxury beach resort located in South Goa operating under the name Park Hyatt Goa Resort & Spa by IFCI Limited to the Company and directed that the hotel property be handed over within six months. The Company obtained possession of the hotel on 19th Sep 2018, and successfully commenced operations under the brand name ITC Grand Goa Resort & Spa from 15th October 2018. With direct access to the pristine Arossim beach, this beach-side, village-styled resort's architecture draws inspiration from the Indo-Portuguese vintage and a distinctive regional allure that's infused in its service, cuisine, rituals and more - promising a truly immersive experience. Reconfigured with the acknowledged ITC Hotels personalised service design and infused with an improved food and beverage portfolio, the hotel has been well accepted by both the domestic and international clients.

Please refer to the Hotels section in the Report of the Directors & Management Discussion and Analysis for the financial year ended 31st March 2018 and Media Releases on quarterly results for further details.

Q20. Please provide an update on the Company’s Agri Business.

Answer:After three successive years of decline, Indian leaf tobacco crop output in 2018 increased by 6 million kgs. to 218 million kgs. However, it still remains far below the levels of 2014 representing a cumulative drop of over 30%. In India, only 10% of tobacco is consumed for cigarettes. Without cognising for this unique tobacco consumption pattern, extremely high rates of taxes are levied on Cigarettes in India which apart from impacting domestic legal Cigarette industry, has also resulted in significant pressure on leaf tobacco crop. This together with declining trend of global cigarette demand and relative strength of the Indian Rupee compared to currencies of competing origins has culminated in reduced demand for Indian tobacco with leaf tobacco exports declining to a decade low of approximately 180 million Kgs.

Despite such challenging market conditions, the Company consolidated its leadership position as the largest Indian exporter of unmanufactured tobacco with further improvement in market standing. This was achieved through new business development and enhanced value delivery to existing customers by leveraging the Business’s expertise in crop development, superior leaf procurement processes and world-class processing facilities. The Business aggressively pursued and acquired new customers to widen the customer base by leveraging long term supply arrangements and collaborative crop development. The Business continued to provide strategic sourcing support to the Company’s Cigarette Business meeting all requirements at competitive prices.

Market opportunities in Wheat and Oilseeds along with enhanced focus on value-added portfolio, especially Coffee, Aqua and Spices, were the key growth drivers during the year. The Business continues to support the growing requirements for Aashirvaad atta delivering substantial savings to the system through deep farmer engagement, sourcing the right wheat varieties, efficient logistics management and other cost-optimisation initiatives.

The Business leveraged its extensive sourcing network and associated infrastructure in key growing areas coupled with deep-rooted farmer linkages to source high quality fruit pulp for the Company’s ‘B Natural’ juices brand. The Business tailored its sourcing and supply chain network to enable migration of the entire B Natural juices portfolio to ‘made with 100% Indian Fruit & 0% Concentrate’ proposition – a first in the industry, benefitting both consumers through higher retention of natural nutrients as well as the Indian farmers.

During the year, the Business also strengthened its milk procurement network for ‘Aashirvaad Svasti’ Dairy Products with significant increase in daily milk collection. During the year, the Business expanded its milk sourcing network to Kolkata for Fresh Dairy Products and to Punjab for meeting the requirement of Dairy Beverages under the Brand ‘Sunfeast Wonderz’. In the Agri Business, the Company remains focused on enhancing its presence in the high value-added segment. Branded frozen prawns and packaged frozen snacks are some of the recent additions in these high value-added segments. The branded prawns under the ‘ITC Master Chef’ range are ‘Super Safe’ frozen prawns which adhere to the same stringent standards prevalent in USA, Europe, and Japan.

The year also marked the Company’s foray into branded packaged frozen snacks under the ‘ITC Master Chef’ brand in select cities for the retail segment, leveraging the culinary expertise of ITC Hotels. The Business continues to expand its footprint in Branded Apples and Potatoes by offering differentiated varieties of low Sugar, antioxidant, baby potatoes and french fry potatoes.

The deep rural linkages and expertise in agri-commodity sourcing resident in the Agri Business, coupled with differentiation through value-added services of identity preservation, traceability and certification is a critical source of competitive advantage for the Branded Packaged Foods Businesses.

Please refer to the Agri Business section in the Report of the Directors & Management Discussion and Analysis for the financial year ended 31st March 2018 and Media Releases on quarterly results for further details.

Q21. Please provide an update on the Company’s Paperboards, Paper and Packaging Segment.

Answer:After a sluggish year in 2017-18 when the industry was affected due to GST transition and ban on sale of liquor in outlets along highways, the Domestic Paperboard, Paper and Packaging Industry, witnessed demand recovery across end-user segments, aided by a favourable operating cycle. The Company’s strategic investments in pulp import substitution, proactive capacity addition in value-added paperboard, process innovations and a cost-competitive fibre chain supported by go-to-market strategies helped deliver robust growth in Revenue and substantial improvement in profitability.

The Business remains a clear leader in the Value Added Paperboards segment and continues to consolidate its preferred supplier position amongst leading end-use customers and brands. The capacity augmentation in VAP segment at Bhadrachalam Mill was completed and commissioned during the year. The machine, equipped with latest technology, is operating at near-full capacity, delivering superior quality board which has been well accepted in the market. The Business sustained its leadership position in the sale of eco-labelled products, volumes of which grew by appx. 33% during the year. In the Specialty Papers segment, the new Décor machine commissioned last year is operating at optimum capacity and the diverse product range has been well accepted by discerning customers.

The Business continues to make structural interventions in the areas of strategic cost management and import substitution. These include augmentation of in-house pulp manufacturing capacity, efficiency improvements of existing equipment and developing alternative sources of supply for key inputs on an ongoing basis. Capacity utilisation of Bleached Chemi-Thermo Mechanical Pulp mill (BCTMP) at Bhadrachalam unit was further scaled up during the year, leading to reduced dependence on imported pulp and thereby cost savings. Innovations in the pulp mill have resulted in higher pulp production and improvement in pulp quality and pulp yield.

The Packaging and Printing Business further consolidated its position as a ‘one-stop shop’ offering a wide range of superior and innovative packaging solutions. With its comprehensive capability-set across multiple platforms, coupled with in-house cylinder making and blown film manufacturing lines, the Business continues to provide innovative solutions to several key customers in India and overseas, catering to the packaging requirements across several industry segments viz. Food & Beverage, Personal Care, Home care, Footwear, Consumer Electronics, Pharma, Liquor and Tobacco. The Business continued to provide strategic support to the Cigarette and FMCG businesses.

Please refer to the Paperboards, Paper & Packaging section in the Report of the Directors & Management Discussion and Analysis for the financial year ended 31st March 2018 and Media Releases on quarterly results for further details.

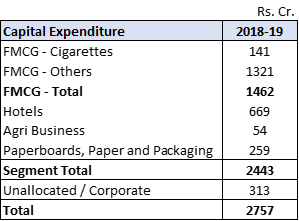

Q22. Please provide details of the Company’s Capital expenditure by Business.

Answer:The Company’s Capex during the last financial years is tabulated below:

Q23. Please provide an overview of the capex plan of the Company.

Answer: The Company’s capex plans are directed primarily towards capacity gearing, productivity enhancement, ensuring the highest standards in quality and environment, health & safety, and R&D.

One of the key elements of the capex plan going forward is to invest in setting up state-of-the-art owned integrated consumer goods manufacturing and logistics facilities across regions in line with long-term demand forecasts. Currently, over 15 projects are underway and in various stages of development - from land acquisition/site development to construction of buildings and other infrastructure.

The Hotels Business made a steady progress during the year in the construction of luxury hotels at Kolkata and Ahmedabad. Construction of ITC Royal Bengal in Kolkata is nearing completion and is expected to be commissioned in the first quarter of 2019-20.

The major items of capital expenditure in the Paperboards, Paper and Packaging segment going forward comprise paperboards capacity augmentation/machine rebuild at the Bhadrachalam unit and capacity augmentation in Cartons and Flexibles packaging at the Tiruvottiyur and Haridwar unit.

Overall, the Company estimates capex of around 17000 Crores over the next 5 years (excluding investments for inorganic growth and acquisition of trademarks, other intellectual property, etc.). However, this would depend on several factors such as pick-up in economic activity and improvement in demand conditions, timely acquisition of land at desirable locations, obtaining approvals from the concerned authorities in a timely manner etc.

Q24. Why has the Segment Capital Employed increased by Rs. 1,775 Crores from Rs. 22,508 Crores as at 31st March 2018 to 24,283 Crores as at 31st March 2019?

Answer:The increase in Segment Capital Employed is primarily on account of capacity augmentation in FMCG Business, ongoing investments in Hotels and cost reduction related investments in Paperboards, Paper and Packaging business coupled with higher inventory in Agri Business.

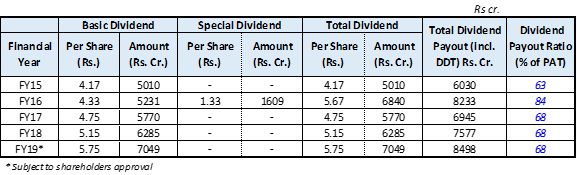

Q25. What are the dividend payout trends in recent years? What is the Dividend policy of the Company?

Answer:Dividend paid out by the Company for the last 5 years is given below:

Please refer to the following link for the Dividend Distribution policy of the Company.

https://www.itcportal.com/about-itc/policies/dividend-distribution-policy.pdf

Q26. Please explain the Company’s ‘Triple Bottom Line’ philosophy.

Answer:Inspired by the opportunity to sub-serve larger national priorities, the Company redefined its Vision to not only reposition the organisation for extreme competitiveness but also make societal value creation the bedrock of its corporate strategy. This super-ordinate Vision spurred innovative strategies to address some of the most challenging societal issues including widespread poverty, unemployment and environmental degradation. The Company’s sustainability strategy aims at creating significant value for the nation through superior ‘Triple Bottom Line’ performance that builds and enriches the country’s economic, environmental and social capital. The sustainability strategy is premised on the belief that the transformational capacity of business can be very effectively leveraged to create significant societal value through a spirit of innovation and enterprise.

The Company is today a global exemplar in sustainability. It is a matter of immense satisfaction that its models of sustainable development have led to the creation of sustainable livelihoods for around six million people, many of whom belong to the marginalised sections of society. The Company has also sustained its position of being the only Company in the world of comparable dimensions to have achieved the global environmental distinction of being water positive (for 17 years in a row), carbon positive (for 14 consecutive years) and solid waste recycling positive (for 12 years in succession).

To contribute to the nation’s efforts in combating climate change, the Company’s strategy of adopting a low-carbon growth path is manifest in its growing renewable energy portfolio, establishment of green buildings, large-scale afforestation programme and achievement of international benchmarks in energy and water consumption. In FY 18-19, about 41% of the Company’s total energy requirements were met from renewable energy sources - a creditable performance given its expanding manufacturing base. The Company is well positioned to benefit from energy conservation and renewable energy promotion schemes such as Perform, Achieve and Trade (PAT) and Renewable Energy Certificates (RECs) promoted by the Government of India. As a responsible corporate citizen, the Company has made a commitment to reduce dependence on energy from fossil fuels. Accordingly, all factories incorporate appropriate green features and premium luxury hotels and office complexes continue to be certified at the highest level by either the US Green Building Council, Indian Green Building Council or the Bureau of Energy Efficiency (BEE).

The Company has adopted a comprehensive set of sustainability policies that are being implemented across the organisation in pursuit of its ‘Triple Bottom Line’ agenda. These policies are aimed at strengthening the mechanisms of engagement with key stakeholders, identification of material sustainability issues and progressively monitoring and mitigating the impacts along the value chain of each Business.

The Company’s 15th Sustainability Report, published during the year detailed the progress made across all dimensions of the ‘Triple Bottom Line’ for the year 2017-18. This report is in conformance with the latest Global Reporting Initiative (GRI) Guidelines - G4 under “In Accordance - Comprehensive” category and is third-party assured at the highest criteria of “reasonable assurance” as per International Standard on Assurance Engagements (ISAE) 3000. The 16th Sustainability Report, covering the sustainability performance of the Company for the year 2018-19, is being prepared in accordance with the GRI Standards and will be made available shortly.

Please refer to the following link https://www.itcportal.com/sustainability/sustainability-report-2018/sustainability-report-2018.pdf for Sustainability Report 2018.

In addition, the Business Responsibility Report (BRR), annexed to the Report and Accounts 2018, maps the sustainability performance of the Company against the reporting framework suggested by Securities and Exchange Board of India.

The Company has prepared its Integrated Report for the financial year 2018-19. As a green initiative, the Report will be hosted on the Company’s corporate website at https://www.itcportal.com/about-itc/shareholder-value/index.aspx.

Q27. Please provide an update of the Company’s Corporate Social Responsibility Programme.

Answer:The Company’s Social Investments Programme aims to address the challenges arising out of poverty, environmental degradation and climate change through a range of activities with the overarching objective of creating sustainable sources of livelihood for stakeholders.

The footprint of the Company’s CSR programme can be viewed at a glance in the following chart:

| Intervention Areas | Unit of Measurement | Cumulative till date |

| Social and Farm Forestry Soil and Moisture Conservation Programme | Acre Acre | 732,903 1,011,601 |

| Sustainable Agricultural Practices Compost Units Sustainable Agriculture Programme | Number Acre | 40,699 394,762 |

| Sustainable Livelihoods Initiative Cattle Development Centres Animal Husbandry Services | Number Artificial Inseminations (in lakhs) | 156 23.67 |

| Economic Empowerment of Women Ultra Poor Women covered Self Help Group Members Livelihoods created | Number Number Number | 22,700 42,057 64,606 |

| Primary Education Children covered | Number (in lakhs) | 6.91 |

| Health and Sanitation Low Cost Sanitary Units Households covered under Solid Waste Management | Number Number | 35,916 211,826 |

| Vocational Training Students Enrolled | Number | 67,496 |